A year after Greece received a €110 billion ($158 billion) bailout package from the European Union and IMF, the resurgence of the European debt crisis serves to illustrate that you can not cure debt with more debt.

Greek debt is on its way to reach 157.7% of GDP this year, and will climb to 166.1% in 2012, according to the forecast by the European Commission (Fig. 1). The country also suffered a fresh sovereign debt downgrade from BB+ to B+ on Friday, May 20 by Fitch Rating, citing significant challenge to secure solvency of the state and sustained economic recovery.

Greek debt is on its way to reach 157.7% of GDP this year, and will climb to 166.1% in 2012, according to the forecast by the European Commission (Fig. 1). The country also suffered a fresh sovereign debt downgrade from BB+ to B+ on Friday, May 20 by Fitch Rating, citing significant challenge to secure solvency of the state and sustained economic recovery.

[Click all to enlarge]

U.S. - Looking Good By Comparison

Across the Atlantic Ocean, the U.S. has its own debt problems as well. The U.S. government hit the debt ceiling of $14.294 trillion on May 16. In the worst case scenario, if the lawmakers do not get it together by Aug. 2, the United States will no longer be able to pay its bills in full. But the general expectation is that the current Congress most likely will not try to make history this time around.

Furthermore, since the U.S. is ahead of Europe in this Great Recession cycle, its economy is also further into the recovery phase. There are signs of increasing consumer spending, which fuels about 60-70% of the U.S. GDP. For instance, in the first quarter of 2011, American Express (AXP), MasterCard (MA) and Visa (V) all reported increases in card spending as credit condition gradually loosens, and consumers start usingcredit cards to build credit again in a slowly healing economy.

Most importantly, there’s a major difference between the U.S. debt situation and that of Europe — the borrowing costs remain reasonable for the U.S. (Fig. 2) and there’s not an insolvency issue.

Risk Off: King Dollar & Gold

Comparing the U.S. with Europe, coupled with some bearish economic data indicating a coming global economic slowdown including the ever-unrelenting China, investors are now piling on risk off trades, selling off equities and commodities and going into the traditional safe havens -- U.S. dollar/Treasury and gold.

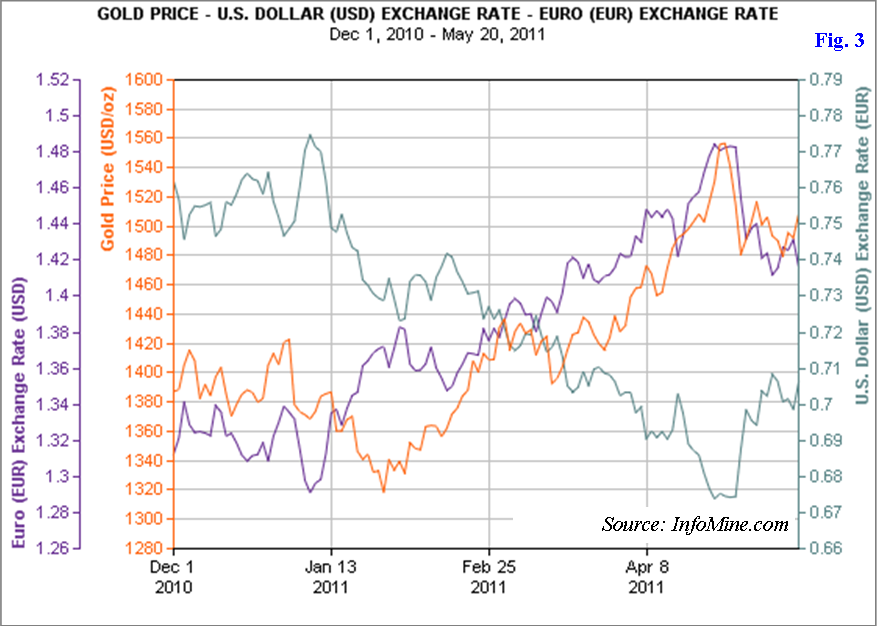

The euro depreciated to less than $1.40 for the first time since mid-March on Monday, May 23, while gold, which typically has an inverse relationship with the dollar, has now flipped into inverse with the euro (Fig. 3).

Chapter 1: Greece

The European debt crisis is set to be the topic du jour in the G8 meeting on May 26-27 in France, and Greece is just Chapter 1 of the European debt saga. Greek austerity measures have been met with intense domestic social and political resistance. But without a system-wide total overhaul and reform, steep budget and spending cuts have failed to restore market confidence. The implied cost of borrowing on 10-year Greek bonds surged to 16.75%, a new euro record, more than twice the rate at the time of the bailout a year ago, while the country’s two-year bond yield is around 25%.

High debt alone is not as bad if there’s enough growth and reasonable bond rates to repay and refinance debts. In the case of Greece, it is highly improbable that it could generate enough growth to afford the sky-high premiums investors are asking to keep its debt afloat (Fig. 1).

Default, Haircut, Bailout or Exit?

Already 85% of international investors recently surveyed by Bloomberg said Greece will probably default, with smaller majorities predicting Portugal and Ireland will do the same. Most economists believe Greece won’t be able to repay its €350 billion debt, so Greece is either going to default or need a new bailout. Many experts estimate a haircut, i.e., reducing the debt principal, of at least 50%, is required to get Greece debt under control.

Another drastic option is for Greece to exit the euro so it can devalue its currency to afford these debts. But that would involve a messy debt conversion process, and most likely a majority of the debt may still need to be paid back in euros.

High Exposure: ECB & European Banks

Further complicating the matter is that because of the bond-buying program put in place last year, the European Central Bank (ECB) is in effect the biggest holder of Greek debt. According to LaRouchePAC(emphasis ours):

Of the €330 billion of Greek debt, 11% of which is now held by European governments (through the EU110 billion bailout package) and the IMF, another 20% is held by the ECB through direct purchases. Greek banks themselves hold EU91 billion, which used this debt as collateral for liquidity from the ECB. Thus the ECB in reality holds a "notional" €200 billion lent to Greek banks. The ECB holds similar amounts of Portuguese, Irish, and Spanish debt. Thus the biggest loser in a 50% haircut on the debt will be … the ECB.

Banks in France, Germany and the UK have the largest exposure to Greek debt (Fig. 4). Goldman Sachs (GS) estimated that a 60% haircut would wipe out as much as 80% of Tier 1 capital at Greek banks. In order to avoid contagion, these banks would need “pre-emptive” capital injections.

Needless to say, a default or a big enough haircut could eventually result in the insolvency of Greek banks as well as the ECB, while causing some potentially serious damage to the entire European banking system.

Chapter 2: Ireland, Portugal, Spain & Italy?

Since Greece is the first of the three euro zone countries accepting the IMF-Europe rescue, given the similar debt and GDP projections (Fig. 1), future crisis could be expected to erupt in Ireland and Portugal, which followed Greece into the bailout fold, as well. In addition, Spain is another promising high debt candidate in line for a bailout, and Standard & Poor’s just cut the rating outlook for another PIIGS country -- Italy -- to negative on May 21.

Clashing Views in Europe

So far, there’s a wide divide within the European Union and the ECB on the Greek debt issue. European finance ministers, admitting rescue has failed, for the first time signaled “reprofiling” Greek bond maturities could be in the cards, i.e., extending Greece’s debt-repayment schedule without changing the principal and the interest rates.

However, ECB officials, clashing with European political leaders, have ruled out a Greek debt restructuring, citing high risk of broad contagion.

Euro Chaos + End of QE2 = Dollar Gain

For now, the markets seem to be pricing in an eventual orderly resolution of the Greek debt crisis. As long as a unified and clear solution remains elusive to the euro zone, the euro would continue to weaken against the dollar, while gold would prosper on fear and uncertainty.

So with chaos in the euro zone -- and as inflation trade comes off with the end of QE2 -- from a technical perspective, the euro most likely would test 1.375 in June, 1.35 in two month, and 1.30 in the next four months, with strong support at 1.35 levels (see chart).

Gold: Caught Between End of QE2 & Euro Chaos

Gold, on the other hand, will be facing conflicting market forces, as the end of QE2 in June is deflationary for gold (Goldman Sachs' new-found risk-on commodity bull notwithstanding), while the European debt crisis buoys gold buying. I'd expect markets to figure out gold's direction in the next four months or so.

From a technical point-of-view (see chart), gold is in an upward momentum at the moment, and the next resistance should be at $1,550 with major resistance at $1,600, which would be a good point to short the yellow metal.

However, overall I think gold will resume the historical inverse relationship with the dollar, barring any end-of-world-like events such as a war or multiple sovereign defaults. On that thesis, look for gold to test the downside of $1,500 in June/July with major support at $1,400. And the time to get out of gold would be when major central banks like the U.S. Federal Reserve and the ECB start to raise interest rates.

source:http://seekingalpha.com/article/271786-gold-and-dollar-pop-on-euro-debt-crisis

No comments:

Post a Comment